3 min read

FEMA, Floods, Fires, and Funding, Oh No!

Natural disasters resulting from hurricanes, floods, wildfires, and earthquakes can strike at any moment, leaving behind a trail of destruction and...

3 min read

Natural disasters resulting from hurricanes, floods, wildfires, and earthquakes can strike at any moment, leaving behind a trail of destruction and...

3 min read

Correction, the title should read 19 storms are coming. At least that’s the prediction released last month by Colorado State University. The Atlantic...

3 min read

The mortgage industry, financial services, and FinTech arenas have all received a boost from technology during struggles to provide relief under...

3 min read

It is hard to imagine that we are approaching the three-month mark for working under COVID-19. Keeping up with industry change as we continue to...

2 min read

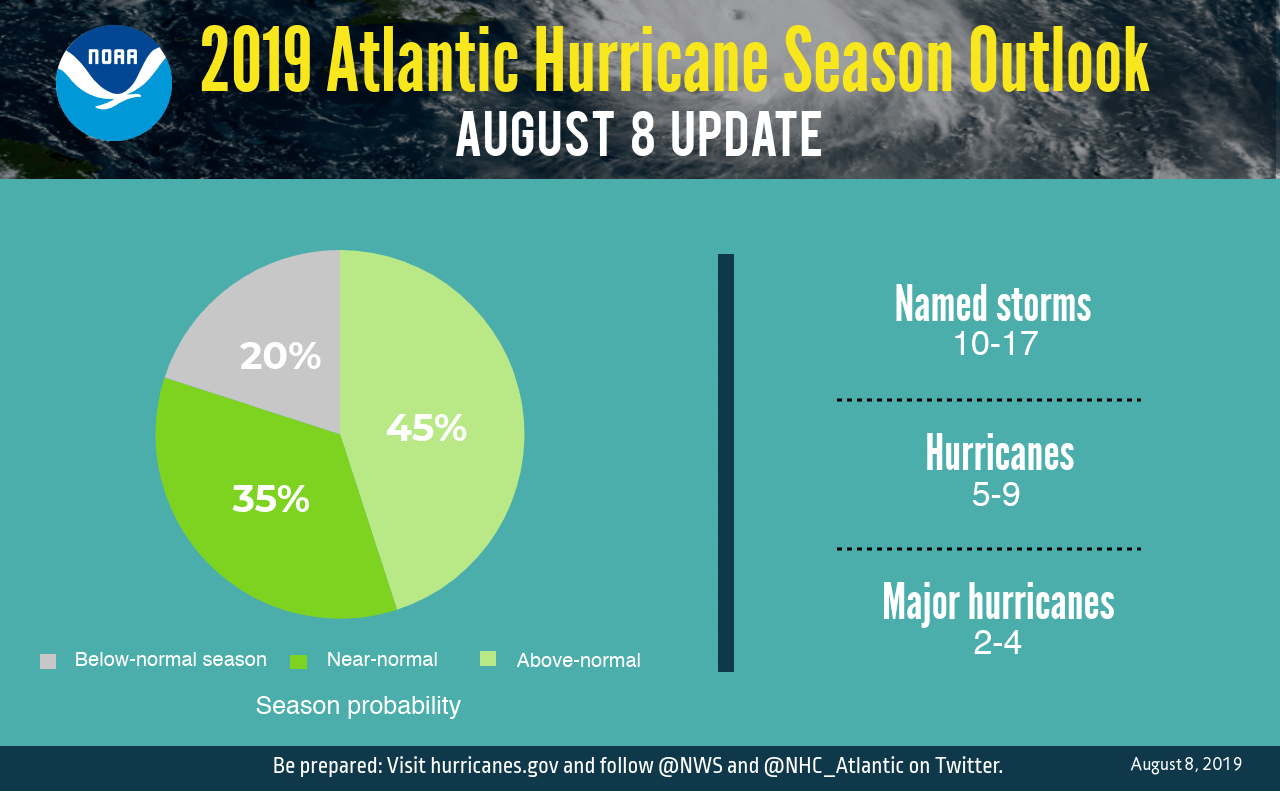

The 2019 hurricane season is already off to a troubling start with Hurricane Dorian having caused an estimated $1.5 billion to $3 billion in...

2 min read

Over the past few months, Clarifire has published meaningful discussions on the numerous requirements mortgage servicers have taken on to manage...

3 min read

Is hurricane season over? Not if you’re a loan servicer. Given the skyrocketing amount of devastation caused by hurricanes, wildfires, flooding and...

3 min read

What does it mean to be disaster ready? As a servicer you’re already juggling a variety of change initiatives at any given time, with unreasonably...

3 min read

The end of this year’s hurricane season is less than two months away; however, with hurricane Florence barely in our rearview, are your operational...